While it might not seem like they have a lot in common, Netflix (NFLX -0.90%) and DocuSign (DOCU -3.72%) have both been in the news lately for less-than-great reasons. And both companies have seen significant drawdowns in their stock prices. Year to date, Netflix is down 70% and DocuSign has dropped 57%.

But investors shouldn't completely lose hope. Both companies still show signs of life -- and potential ahead -- that could make their shares intriguing opportunities now for investors.

So which of the two stocks is the better buy? Let's dive into recent news and earnings results to see.

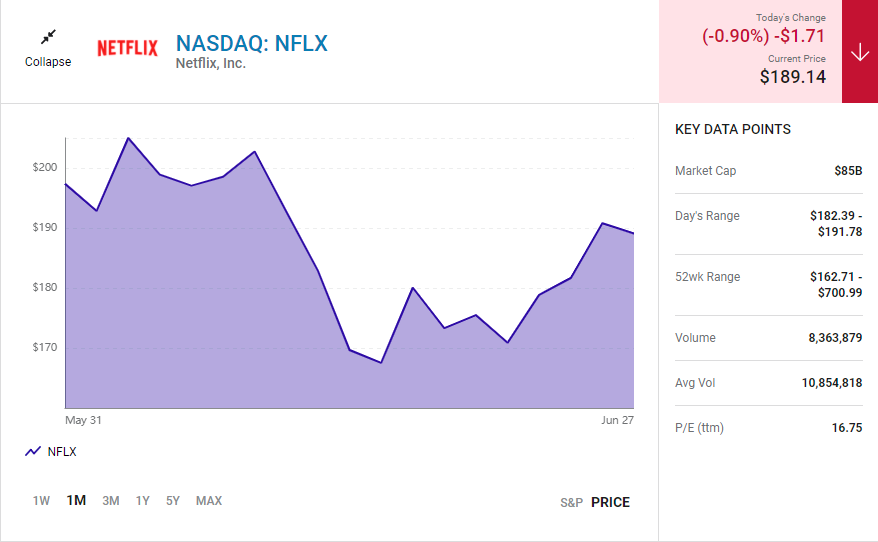

When Netflix reported its first-quarter 2022 earnings in April, the market reaction was swift, with shares falling more than 37%. The headline from the report was that for the first time in over a decade, the company had lost subscribers sequentially.

Although both revenue growth and subscriber growth had been slowing over time, it seemed that this was the tipping point for Wall Street and that the increased competition seen over the past several years was finally catching up to Netflix.

The company did identify a few levers for reversing this trend, which provided some hope. It continues to focus on creating content for international markets, as opposed to simply exporting American-made content.

Netflix believes this is the better way to grow its international business and points out that over half the world's homes don't yet have broadband internet. While it may have reached a saturation point domestically, that's not the case globally.

Management also addressed the issue of password sharing, stating that over 100 million households use another household's account. Netflix is testing new pay structures in a few Latin American countries as a pilot to try to capture some of that lost revenue.

It remains to be seen if this will be rolled out more broadly, and if it will result in increased subscriptions or increased churn.

There has long been speculation about whether or not Netflix might eventually create an ad-supported subscription at a lower price point as a way to grow subscribers.

For the first time, management said during the latest earnings call that it's exploring this as an option, and more recently co-CEO Ted Sarandos confirmed that the company is in talks with several potential advertising partners.

I don't expect Netflix to return to the hypergrowth seen previously, but at the current valuation (the company had a price-to-sales ratio of 2.7 at the time of this writing), there's a larger margin of safety for investors than we've seen in a long time.

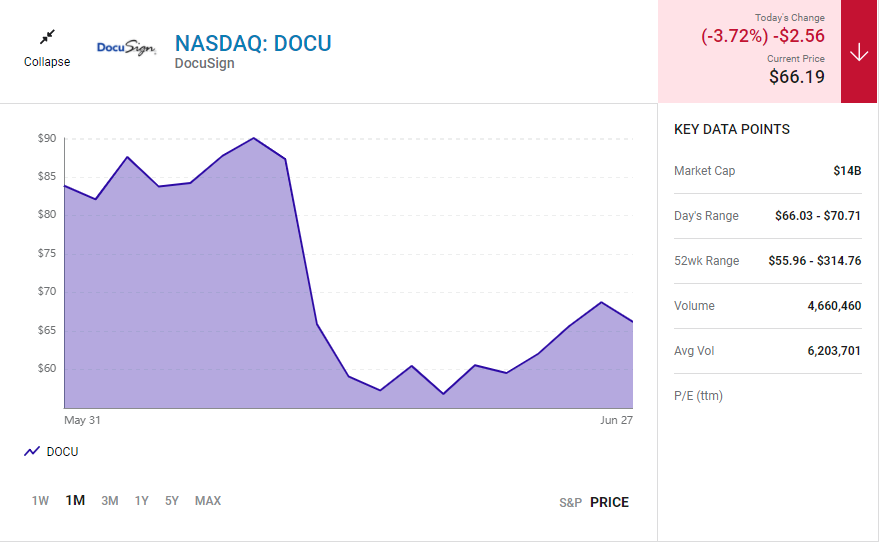

While not quite as drastic as Netflix, DocuSign has also seen a rough post-earning reaction, with shares closing down 25% on the day after its fiscal first-quarter 2023 earnings report. Despite relatively strong growth in revenue, billings, and total customers, each of these metrics represented a deceleration from previous quarters.

DocuSign also missed earnings guidance, with non-GAAP earnings per share (EPS) coming in at $0.38, while analysts were expecting $0.46. On a GAAP basis, the net loss per share was $0.14, compared to a loss of $0.04 in the first quarter a year ago.

Much of this GAAP net loss is attributable to stock-based compensation (SBC), but management stated this might be changing in the future as more employees are seeking guaranteed salaries over SBC.

On the positive side, DocuSign remains a cash-generating business. In the first quarter, it produced $196 million of cash from operations and $175 million of free cash flow.

This represented a continuation of a trend as DocuSign has generated almost $500 million in free cash flow over the past three years.

Investors should keep an eye on the balance between DocuSign's profitability and cash generation. If SBC expenses decrease, that will benefit the bottom line, but will also negatively impact the company's cash flow.

An additional wrinkle has been introduced to DocuSign's investment potential: Just this week it was announced that CEO Dan Springer was stepping down immediately.

The company named an interim CEO and announced plans to conduct a search for a permanent replacement. This complicates the thesis a bit and might warrant taking some time for the management search to play out before making any big bets on DocuSign.

Both companies have deserved some, if not all, of their stock price depreciation over the past few months. That said, both are still leaders in their space. Netflix still has a wide lead in streaming subscribers, and DocuSign remains the market leader in digital signatures.

Considering the headwinds facing both companies, I think DocuSign might be the better buy right now. Even with the uncertainty around the CEO position, DocuSign's cash generation provides a cushion for both the business and investors that make it worth taking a position in the stock.

Hot Topics

Wall St Week Ahead Bruised U.S. Stock Investors Brace For More Pain In Second Half Of 2022

Costa Rica Asks IMF For $700 Million From New Sustainability Trust

Stock Futures Rise As Wall Street Looks To Snap Losing Streak

Investors should watch closely for growth to remain steady or accelerate, and for DocuSign to begin to move toward profitability without drawing too much on its cash. Source: The Motley Fool...